News and Insights

Be Careful What You Wish For: Conquistadors & Cryptocurrencies

February 14, 2020

The Spanish and Portuguese colonization of the New World beginning in the fifteenth century had enormous consequences there as everyone surely knows, but with respect to the central goal of the conquistadors — getting gold and silver, and bringing it back to Europe — they were very successful. Over the next two hundred years, the conquistadors brought back several hundred tons of gold and thousands of tons of silver.

However, there was another consequence to what at first seemed a very straightforward success for the Europeans; because the money used in Europe at the time was gold and silver, such a sudden influx of the supply led to an economic shock so powerful it has a name: the Price Revolution. Inflation skyrocketed, and as the prices of food and other basic goods increased accordingly, hunger and political unrest spread across Europe.

If the same thing happened today, though — an enormous stockpile of gold and silver were discovered; say, it turned out the moon was made of the stuff — the effect on our money would be negligible. Jewelry would suddenly be a lot cheaper, but the amount it cost you to buy a bagel for breakfast, your rent, etc — that would all be essentially unaffected, and that’s because of Richard Nixon.

In 1971, to address several economic issues, Nixon announced that one U.S dollar was no longer worth the equivalent in gold, and this also has a name! The Nixon Shock. Quite rapidly, the value of the U.S. dollar untethered from the value of gold, other countries followed suit, and now the value of money is essentially derived from the trust you have in that particular government to continue running society smoothly. Given current events, that might feel kind of worrisome when you say it out loud.

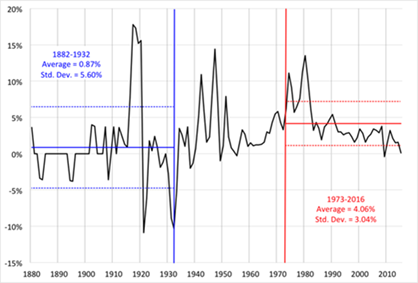

Yet, the untethering of money from gold has worked out very well from an economic standpoint for the same reason the conquistadors learned — life is hard enough without having your money change in value all the time. Look at the below chart of inflation/deflation and you’ll see that price changes in the U.S. are about one-fifth* of what they were before the end of the gold standard:

Source: Federal Reserve Bank of Minneapolis

OK, great — so how do cryptocurrencies come into play? Well, for the first time ever, there is now a technology, blockchain, that allows anyone to 1) create their own money too — since again, money isn’t tied to anything “real” anymore, or at least, physical — and 2) prove to other people that you, the creator of this money, cannot tamper with it, so there can’t be any funny business. As of writing, one Bitcoin is about $10,000, so it seems like this is an appealing idea to a fair amount of people.

Would it surprise you to hear there are still some wrinkles to iron out? For starters, there’s hundreds of cryptocurrencies, and I think we can all agree that the best thing about regular money is that it works everywhere. It’d be pretty annoying to have to pay for your donuts with Dunkin Donuts Dollars, and then convert them to Bonobos Bucks to buy clothes, etc. There are also other issues like the fact that, if no one controls the money, and you lose your password, you therefore lose all your money forever.

These seem like important hurdles, huh? A question we get a lot at Finn Partners while representing cryptocurrency & digital asset businesses is: why bother? As the above chart shows, regular dollars seem to be working pretty well; the economy is great right now … why fix what’s not broken?

Worldwide, there are many different motivations behind cryptocurrencies, but in general you can probably lump the underlying interest into two buckets:

1) A lot of people are having a hard time articulating a concern they have, that, as regular money becomes increasingly digital, it feels less like they own it, and that rubs some of us the wrong way. In the most harmless sense this manifests itself in ways like restaurants no longer accepting cash; in some countries like those in Scandinavia, that’s now true almost everywhere. Going forward, though, if every payment big or small ultimately needs your bank’s approval, and you have no recourse of switching to cash, that once-innocuous checking account provider might start to feel like the arbiter of your life.

2) A very underreported phenomenon, it seems, is nation-state interest in cryptocurrencies. Many U.S. citizens might not understand the degree to which the rest of the world is run on U.S. dollars — but other countries do, and they are not all super pleased with the arrangement. A great example of this was a recent trial in which a Lebanese businessman was accused of funneling bribes to the Mozambique government — and the trial took place in Brooklyn. Why? Because the alleged bribes were paid in U.S. dollars, and those dollars ultimately went through banks based in New York. Around the world, people primarily use dollars to pay for things, and those dollars at some point usually go through the United States, giving our currency a power other countries appear keen to mitigate.

So, yes, cryptocurrencies have many problems at present that need to be fixed. But, there are some very strongly held concerns about the existing monetary system, and generally speaking, imperfect solutions don’t stop collective willpower. Like the conquistadors a half-millennia earlier, U.S. policymakers resoundingly achieved their primary goal by ending the gold standard, but the unintended consequences might be what’s remembered in the end.

*Excepting the inflation in the 70s Nixon was trying to fix